Without the premium that big banks charge for floating rates, they can actually be cheaper than fixed.

Low floating rates aren’t common in NZ. The big banks set their floating rates with a big premium, so people aren’t used to thinking of them as an option to save money. But, low floating rates like Indi’s can be even cheaper than fixed rates. To understand how low floating rates can actually save you money there are two aspects to consider.

- First, a low floating rate like Indi’s should save you money compared to fixing for a year (or 2 years) with a bank. We’ll discuss how Indi’s pricing philosophy is designed to save you money under all interest rate conditions.

- Second, to get payment flexibility, many people have a structured loan with some portion on floating or revolving at a much higher cost. Check out our article to understand how this increases the total cost of your mortgage to be higher than you may realise.

Cheaper than a fixed rate over a year

Indi’s pricing philosophy is to have a floating rate that is at least 0.20% cheaper than the big bank fixed rates over the next year on average.

This doesn’t mean that Indi’s floating rate will always be lower than the big bank fixed rates at any given point in time. It depends on the direction interest rates are expected to move over the next year, especially the official cash rate (OCR) set by the Reserve Bank.

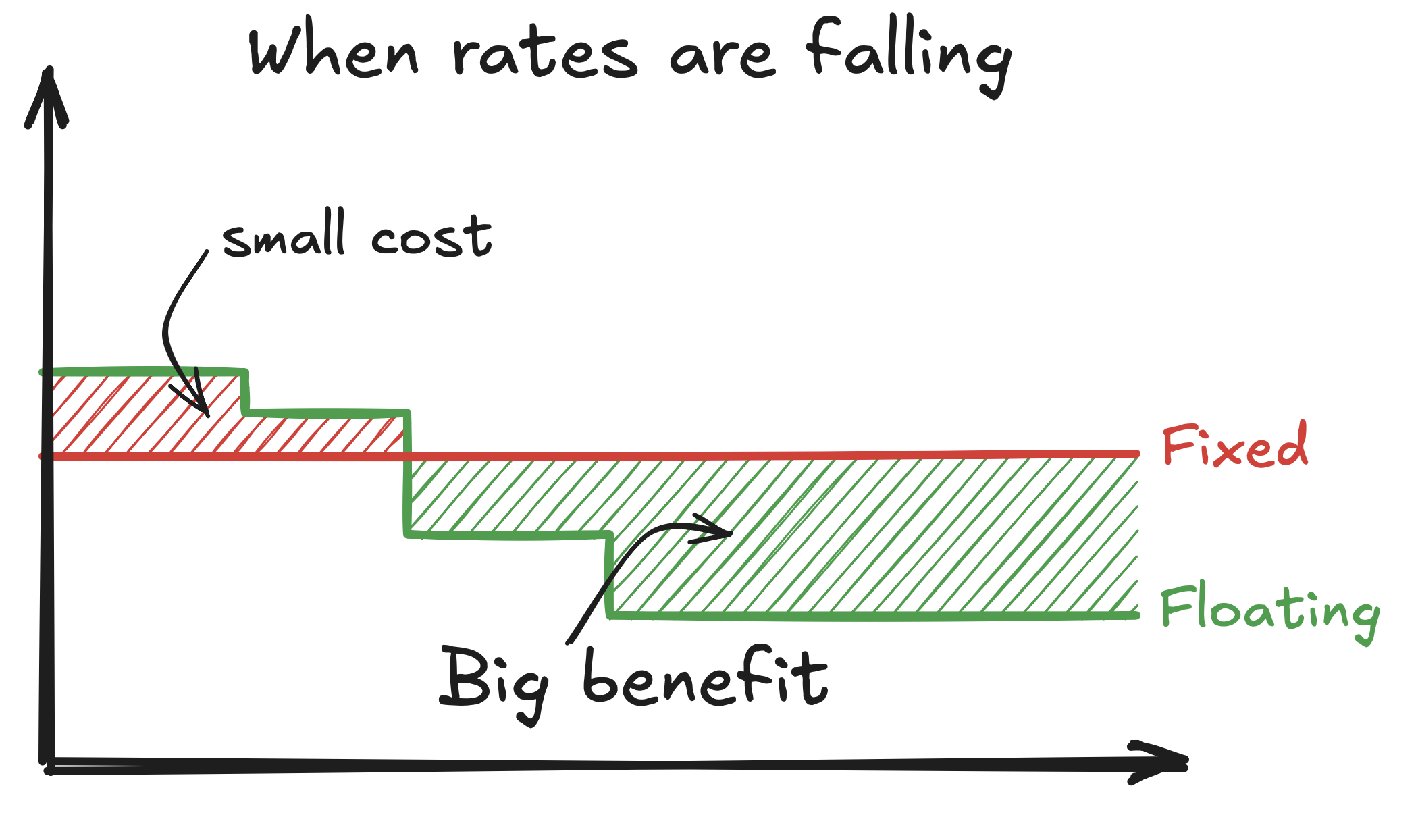

When interest rates are falling, Indi’s floating rate will initially be a bit higher than fixed rates. This is because you’d get that fixed rate for the whole next year (or two years), but Indi’s floating rate will decrease each time the OCR decreases. So although Indi’s rate may start higher than the fixed rates, it will end up lower than the fixed rates after the OCR cuts. Over the year you should save money, on average.

When interest rates are falling, floating rates mean that you get the advantages of OCR cuts as they happen. You can ride rates down.

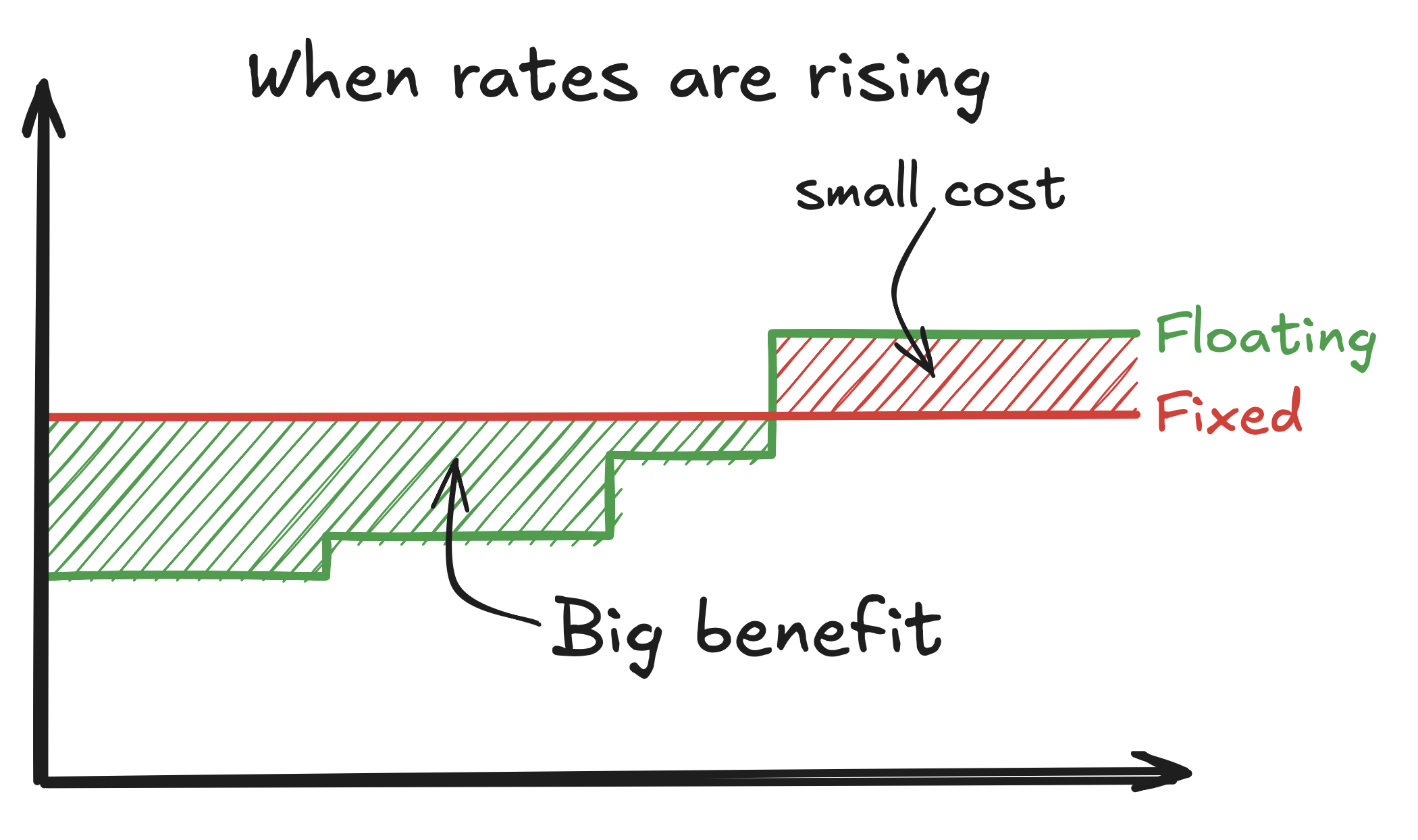

When interest rates are rising it can be a bit scary, and it’s tempting to rush for the certainty of fixed rates. However, you can still save money on average over the year with floating rates, just in reverse. At the time you’re making your choice, floating rates will be lower than the big bank fixed rates. For the first part of the year you’ll be saving money, and in the second part of the year when the floating rate rises it may end up higher than the rates you could have fixed at. At Indi, we set our pricing so that you should save money on average over the course of the year.

Disclaimer: Indi reserves the right to change floating rates at any time and does not guarantee savings in comparison to any other rates. Market conditions can change unexpectedly, which may result in different outcomes than expected. Nothing in this article is financial advice. Indi does not provide financial advice, and recommends you consult an advisor if you have questions or concerns.